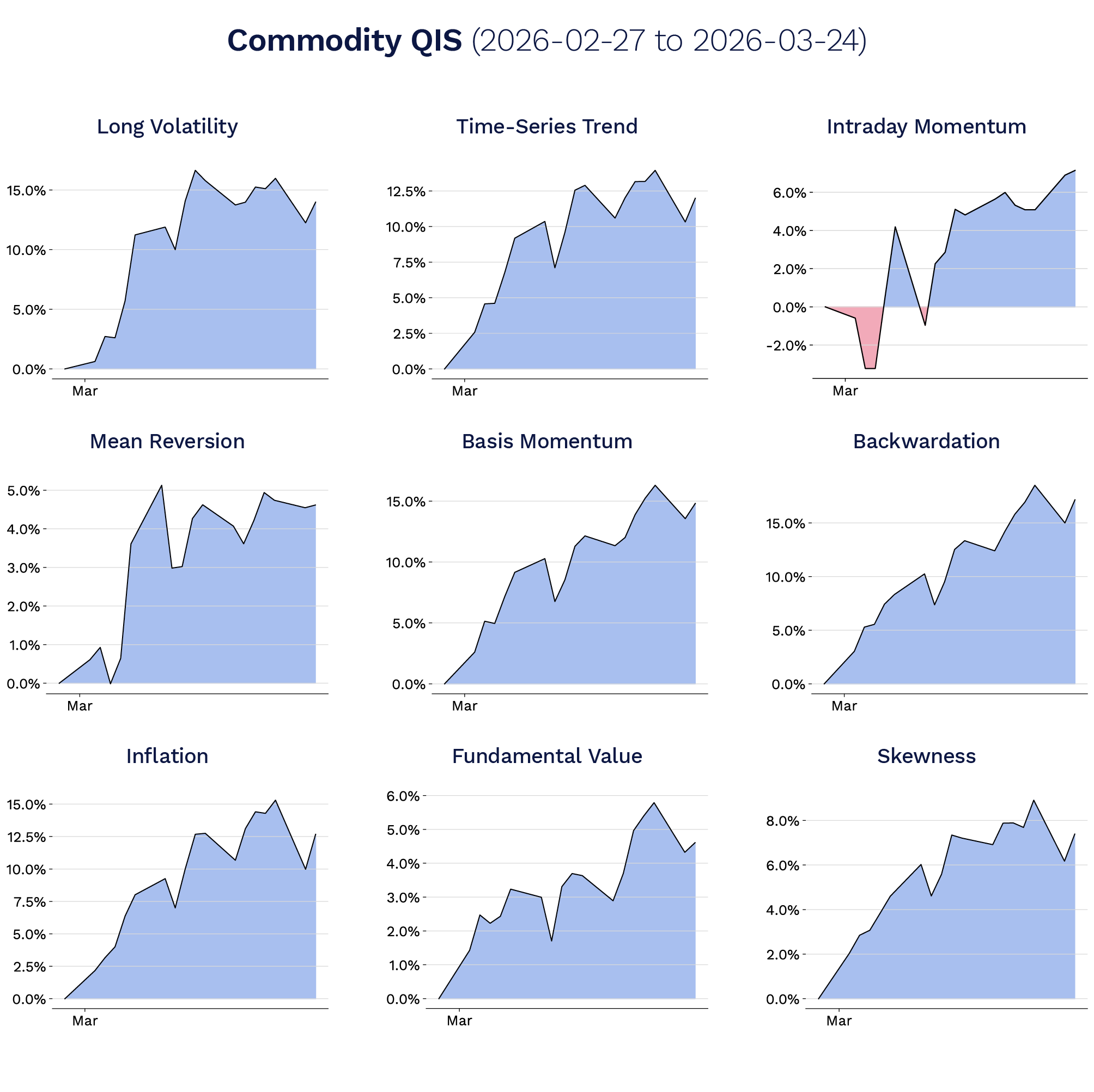

Since the onset of the Iran conflict, the defensive segment of QIS has operated in a market regime defined by downside equity risk, firmer volatility premia, commodity-led macro repricing, most visibly, with Brent crude rising ~90% from recent lows, and less stable cross-asset relationships. In that environment, the strongest performers have been strategies systematically designed to add convexity, preserve downside participation, or monetize stress-driven dislocations.

Across asset classes, positive contributions have come from equity protection overlays, rates volatility and front-end trend, credit widening hedges, FX convexity and carry dispersion, commodity trend and curve-shape exposures, and diversified cross-asset trend frameworks. Collectively, these strategies demonstrate how defensive QIS can function as a rules-based shock absorber when macro and geopolitical stress transmits simultaneously across equities, rates, credit, foreign exchange, and commodities.

In this case study, we examine over 30 different QIS strategies across multiple asset classes.